Through 2020 and 2021, there was an exceptionally high demand for housing due to a homebuying frenzy sparked by record-low mortgage rates and large personal savings. However, things have altered rapidly in recent months. The housing industry isn’t collapsing, but demand for mortgages has decreased dramatically from the start of 2022 due to rising rates and consistently high property prices.However, the amount of debt owed by Americans on their mortgages is $12.14 trillion, making up 70.2% of all consumer debt in the country. The demand for mortgages hasn’t decreased despite interest rates remaining at 7.00%, and people all throughout the nation are still attempting to make their way through the difficult housing market of today. For this reason, an understanding of American mortgage behavior is essential to understanding the status of American financial affairs.

Unpaid Mortgages

Two factors have contributed to the drastic rise in the amount of outstanding mortgage debt: an increase in the number of borrowers and an increase in the average size of mortgages.Many buyers were able to take advantage of cash-out refinances or raise their purchase prices thanks to historically low mortgage interest rates, all while keeping their monthly payments comparable to what was previously offered on lesser loan sizes.

Mortgage Interest Rates

2009 saw the first rate decrease below 5% in the previous 50 years as a result of the Federal Reserve’s aggressive target rate reductions in response to the Great Recession of 2007–2009. In late 2011 and 2020, rates fell below 4% and below 3%, respectively, for the first time.The first week of 2021 saw the lowest level of average mortgage rates (2.65%). November 2001 saw the lowest weekly rate (6.45%) in the thirty years between 1972 and 2001. However, August 2023 saw the return of weekly average mortgage rates above 7.00% for the first time since November 2022. The week of October 26, 2023, saw an average of 7.79%, the highest in almost 20 years.

Originations of Mortgages

Mortgage originations had a sharp decline as interest rates increased from their historic lows in 2021. In actuality, there were $2.75 trillion in mortgage originations in 2022 as opposed to $4.51 trillion in 2021. With $1.1 trillion in originations in the first three quarters of this year compared to $2.2 trillion in the same period last year, 2023 is on track to slash 2022’s amount in half.The yearly origination volume in 2021 was the highest in the previous 20 years, coming in at $4.51 trillion. That year’s historically low interest rates allowed borrowers to take out larger loans with comparable monthly payments, and they also encouraged many to refinance their current mortgages.

Average Loan Amount When Buying a House

The amount borrowed for buying a property differs substantially depending on the area and the cost of homes there.In the 12 months ending in October 2023, the average amount borrowed on our platform to buy a home (excluding down payments and closing costs) varied from $464,994 in Hawaii to $150,245 in West Virginia.

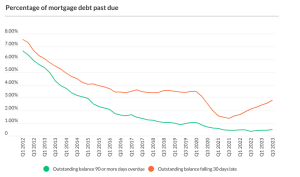

Repossessions and Delinquencies

Nearing a record low, the proportion of mortgage debt that is substantially delinquent—that is, 90 days or more past due. It’s crucial to keep in mind that this indicates the percentage of outstanding debt rather than the total number of accounts.As previously mentioned, super-prime borrowers accounted for a historically high share of the massive increase in total dollars issued as mortgage debt in 2021, which should reduce the amount of debt that falls into delinquency or default.But there’s a reason to be concerned about the future. The level of mortgage debt that fell past due by 30 days started to increase by the end of 2021 after high declines throughout the epidemic.

Who is Best Suited for Adjustable-rate Mortgages?

An ARM could save you money on interest payments if you don’t intend to remain in your house for more than a few years. If you’re still living in the house, you should be prepared to accept a certain amount of risk that your payments may go up. Examine rates on ARM loans.

Different Kinds of Mortgages

Other sorts of mortgages that you may come across when looking for a loan include the following frequent categories:

Loans for Construction

A construction loan, particularly a construction-to-permanent loan that becomes a regular mortgage once you move into the house, can be an excellent financing option if you wish to build a house. The best borrowers for these short-term loans are those with larger down payments.

Mortgages With no Interest

In an interest-only mortgage, the borrower pays principal and interest after making interest-only payments for a certain amount of time, typically five or seven years. With this loan, you won’t accumulate equity as quickly because you’ll only be making interest payments at first. The ideal borrowers for these loans are those who can afford the increased monthly payments in the future or who know they can sell or refinance.

Concurrent loans

An 80/10/10 loan, sometimes known as a piggyback loan, consists of two loans: one for 80 percent of the cost of the house and another for 10 percent. For the remaining 10%, you will pay a down payment. These loan options come with two sets of closing expenses but are intended to help the borrower avoid having to pay for mortgage insurance. Additionally, you would be paying interest on two loans, so this non-traditional arrangement is best suited for people who will truly save money by adopting it.

Balloon Loans

A sizable payment is needed for a balloon mortgage at the conclusion of the loan term. Usually, for a little period of time—such as seven years—you will make payments based on a 30-year term. You will have to make a sizable payment on the remaining amount when the loan term expires, which could become overwhelming if you’re not ready. The best borrowers for these loans are those who can afford to make a sizable balloon payment at the end of the loan period because they have steady financial resources.

Portfolio Financing

Some lenders decide to leave their loans “on the books,” or in their portfolio, while the majority sell them to investors (more on that here). The lender is exempt from FHFA and other regulations as they retain ownership of these loans. They may therefore have more accommodating qualifying standards.

Mortgages for Renovations

You can utilize a renovation loan to buy a house that requires a lot of repair. These loans combine the mortgage payment for both the purchase and the renovation.

Medical Loans

Even with a well-paying career, it can be difficult for doctors to qualify for a standard mortgage because they frequently have significant debt from medical school. Enter physician loans, which facilitate property ownership for medical personnel such as doctors and nurses.

Loans That Don’t Qualify

Non-qualifying mortgages, also known as non-QM loans, have more relaxed credit and income requirements because they don’t adhere to certain regulations established by the Consumer Financial Protection Bureau. A borrower with certain conditions, like erratic income, would find this appealing. On the other hand, some non-QM loans have greater interest rates and down payments.

How to Pick the Best kind of Mortgage Loan for Your Needs

You may be eligible for more than one kind of mortgage, depending on your financial situation and credit history. Similarly, you may be able to cross out several loan categories right away. For example, if you or your spouse have never served in the armed forces, you are not eligible for a VA loan.

Government National Mortgage Association

In the US, mortgage lending is a significant industry, and many of the requirements that loans must fulfill are designed to appease mortgage insurers and investors. As debt securities, mortgages are freely transferred and assigned to other holders. The federal government of the United States established a number of initiatives, or government-sponsored businesses, to promote home ownership, development, and mortgage lending. These programs include Federal National Mortgage Association (Fannie Mae), Federal Home Loan Mortgage Corporation (Freddie Mac), and Government National Mortgage Association (known as Ginnie Mae). These schemes function by providing a mortgage payment guarantee on specific loans that comply. After that, these loans are packaged and sold to investors at a marginally reduced interest rate; these products are referred to as mortgage-backed securities (MBS).

Mortgage Financing That is Predatory

The United States is concerned about the prevalence of predatory mortgage lending among its consumers [1]. The primary worry is that legitimate mortgage lenders and brokers are taking advantage of legal gaps in order to make more money. The usual situation is that the borrower is ignorant and poorly informed, and the terms of the loan exceed their means. After making several main and interest payments, the borrower eventually fails. After that, the lender seizes the asset and collects the whole loan amount, keeping the principal and interest payments together with the loan origination costs.